|

|

Important tax report changes — new rules for managed investment trusts

|

|

|

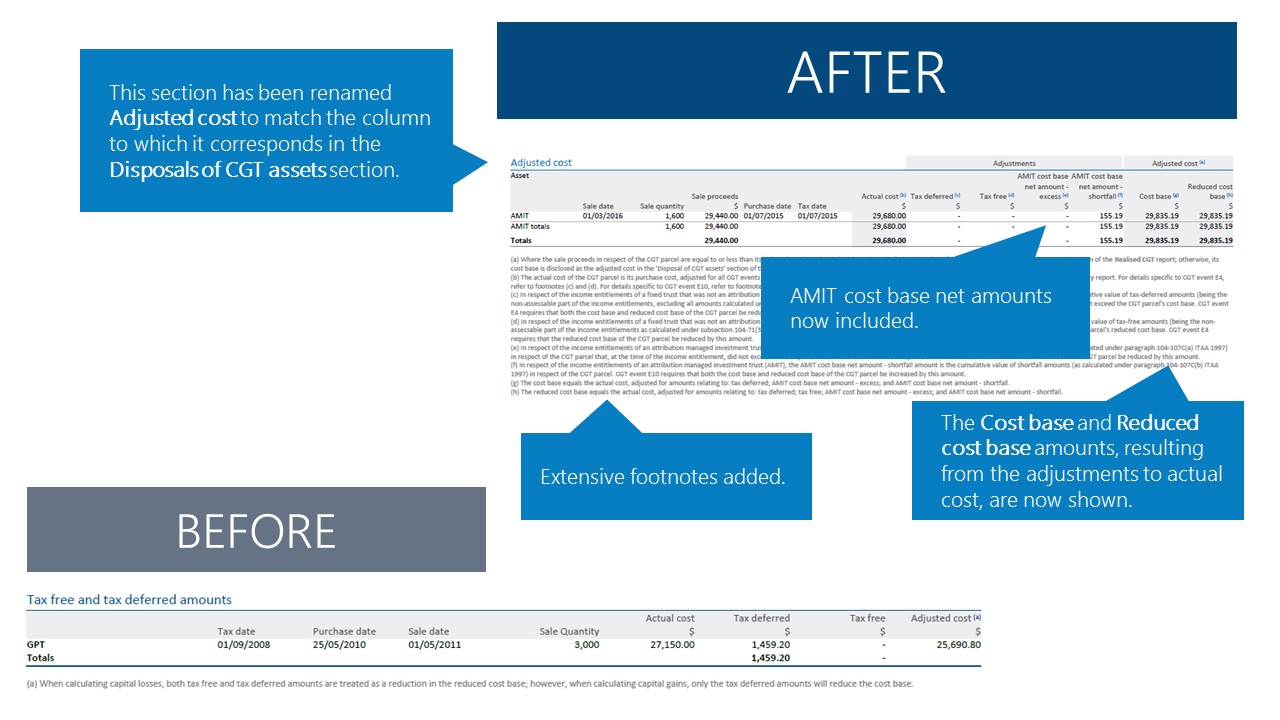

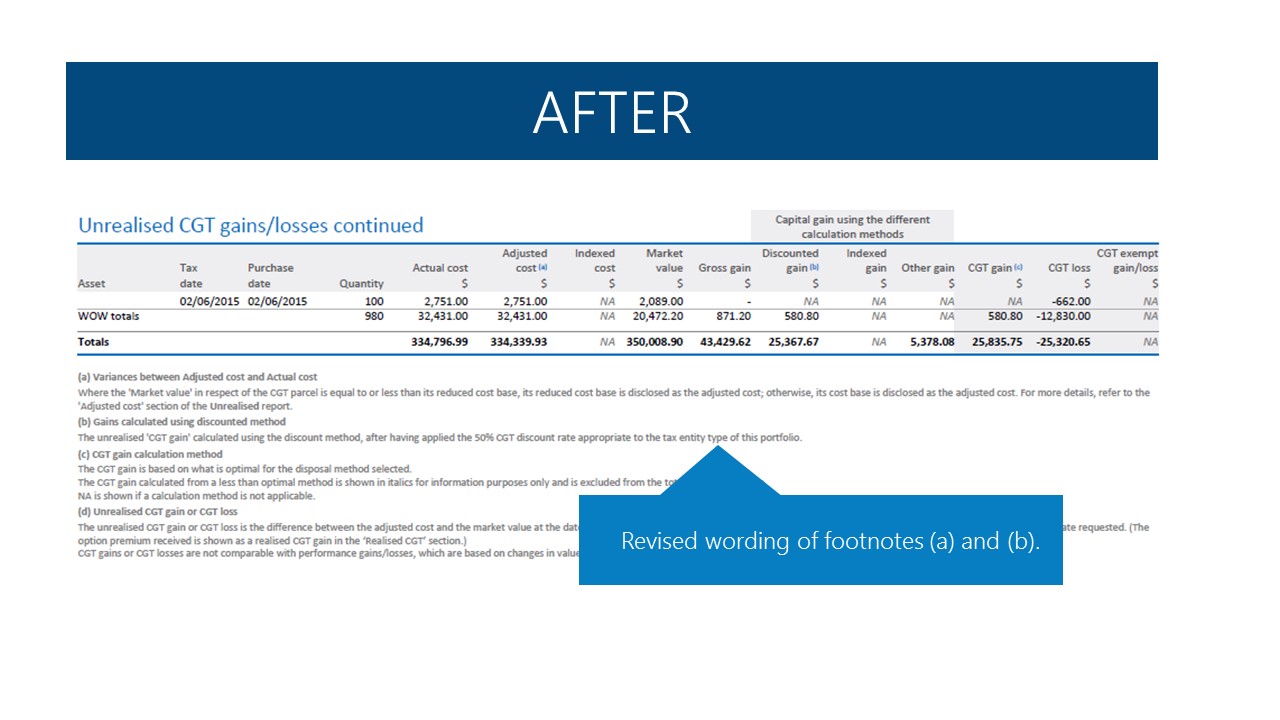

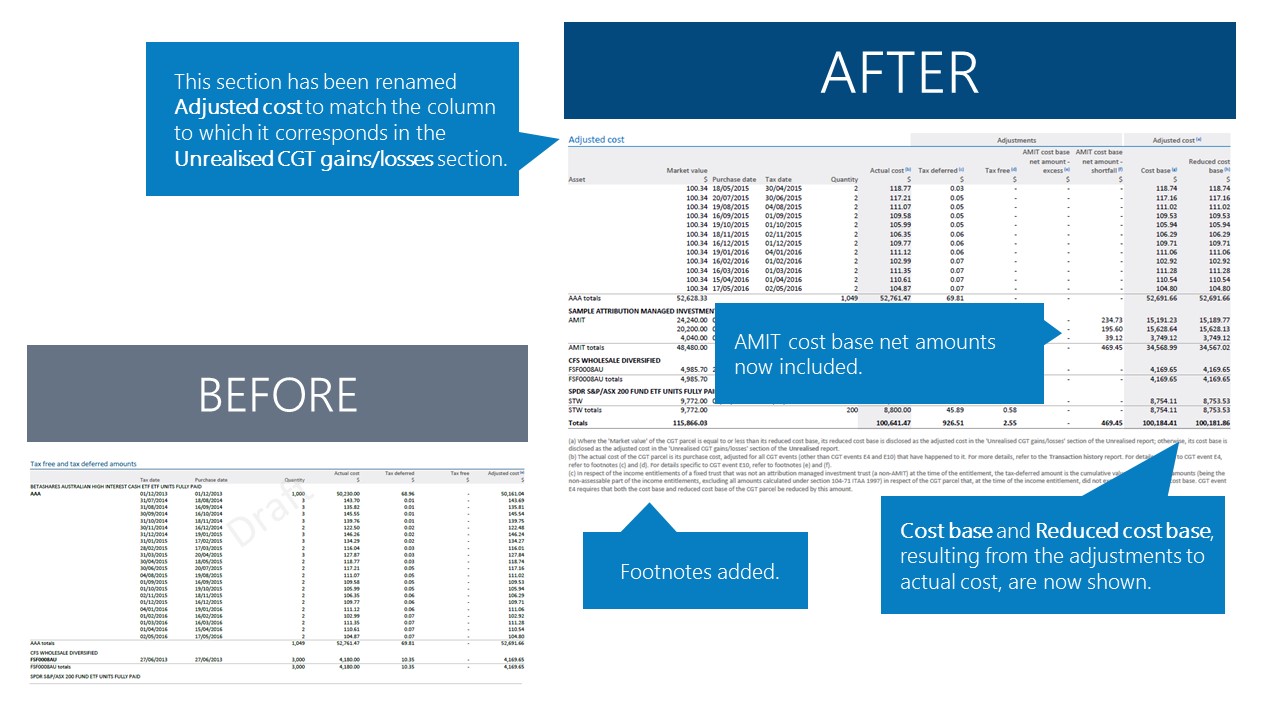

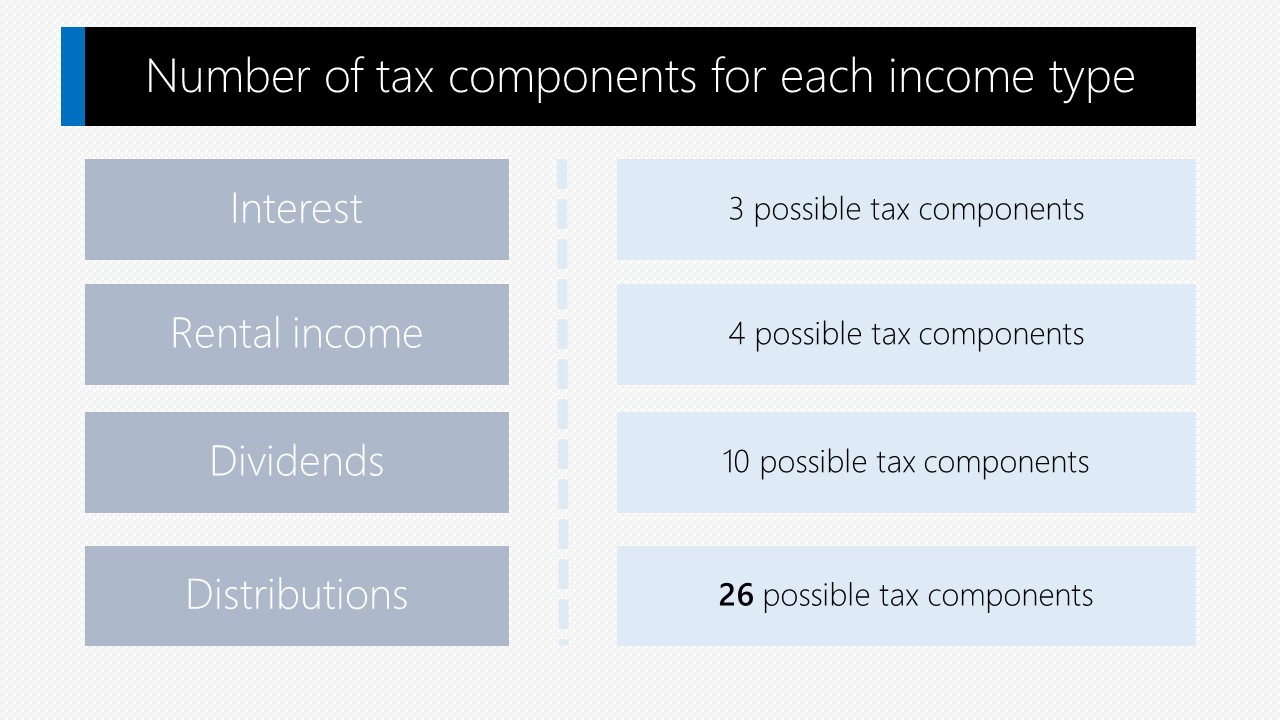

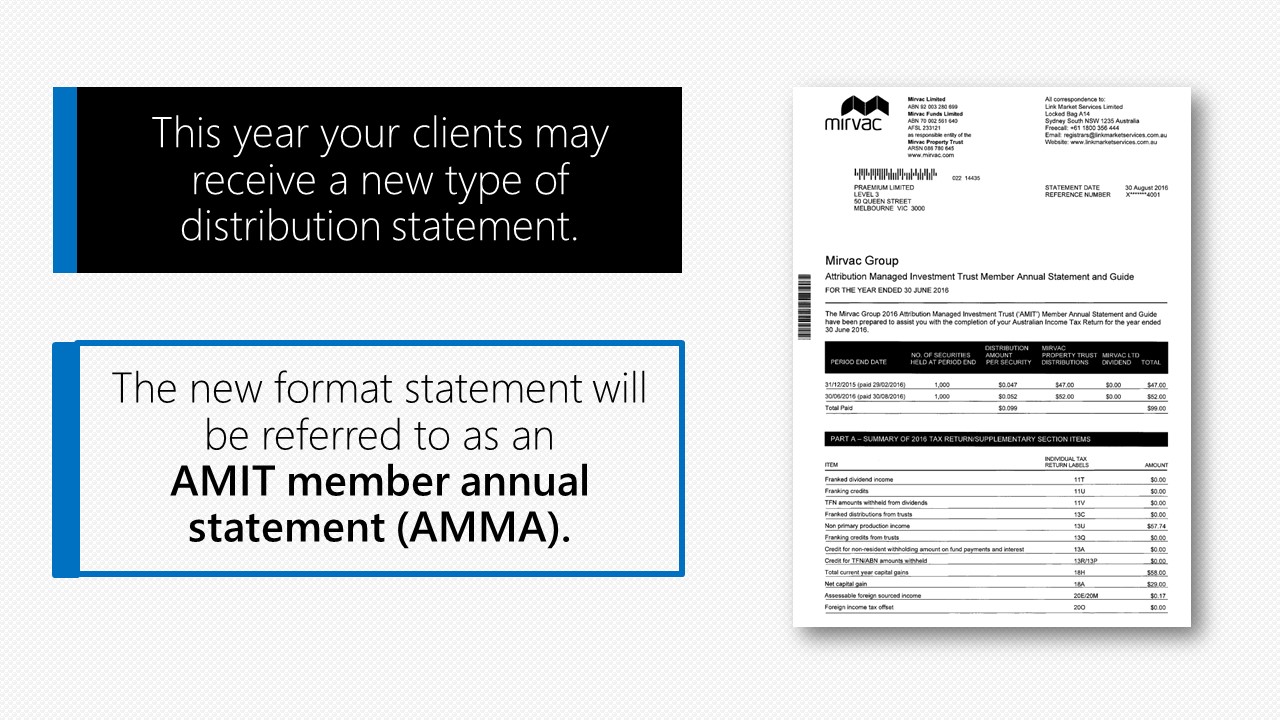

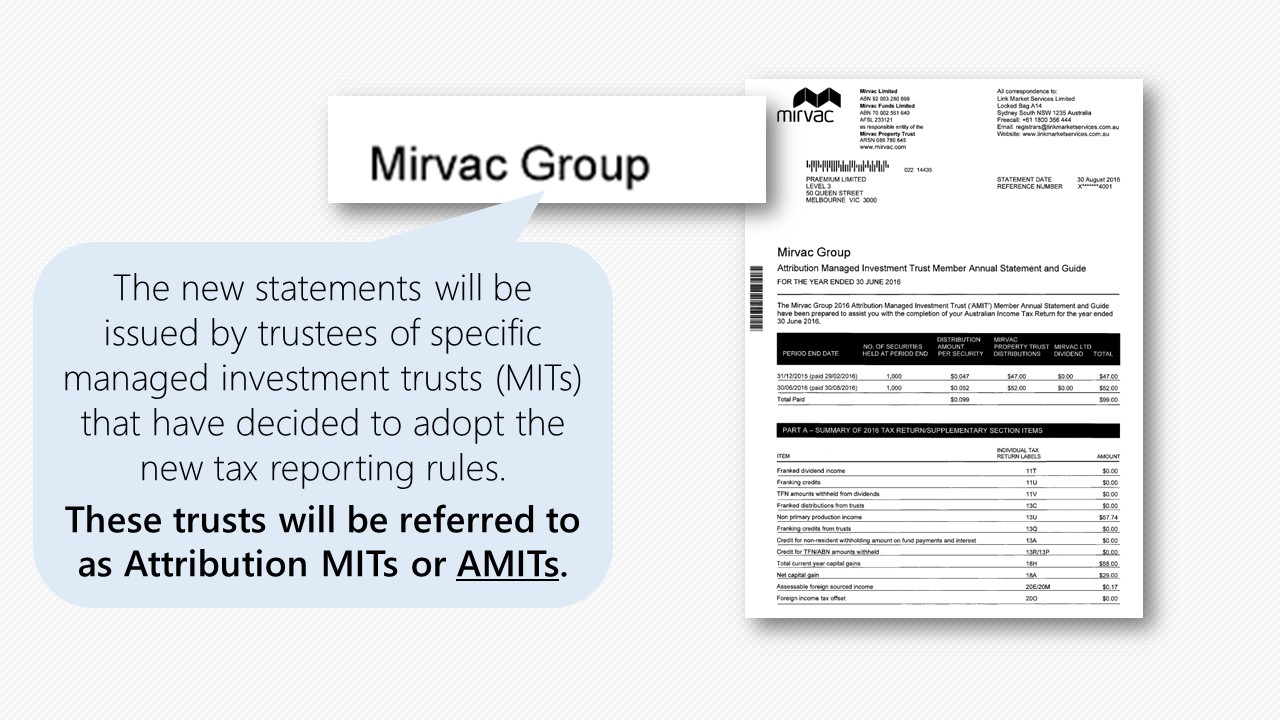

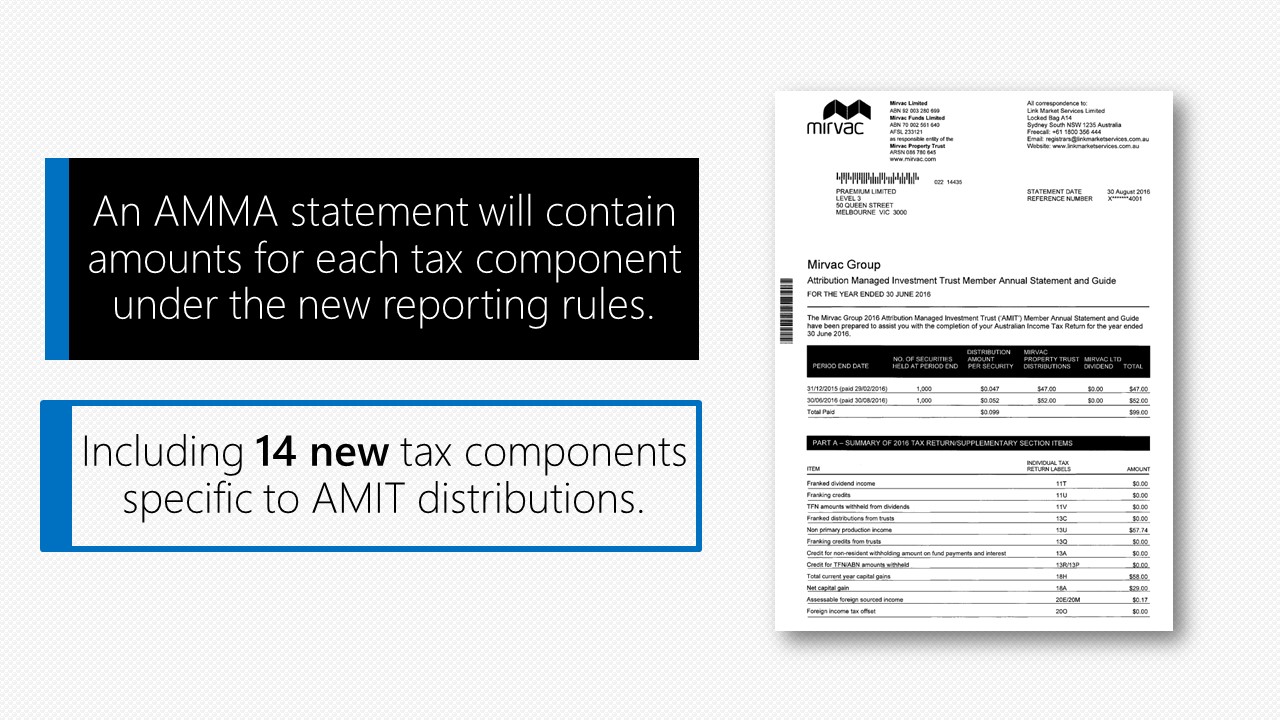

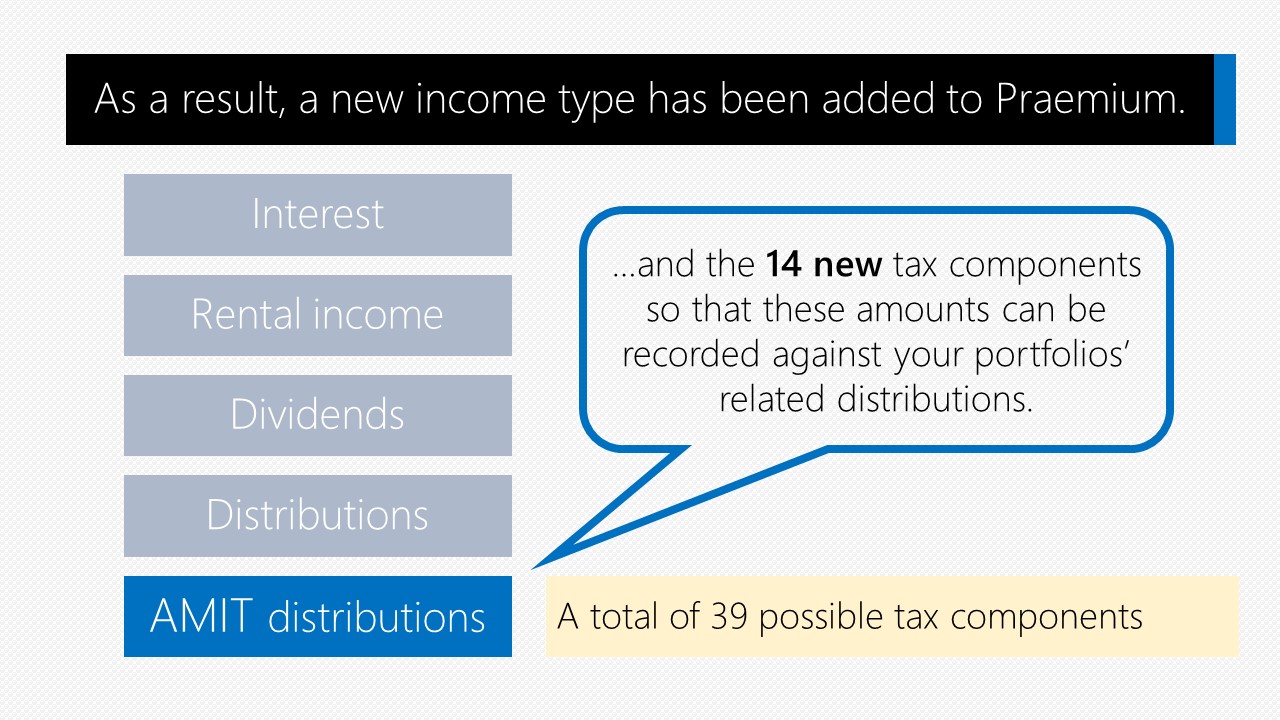

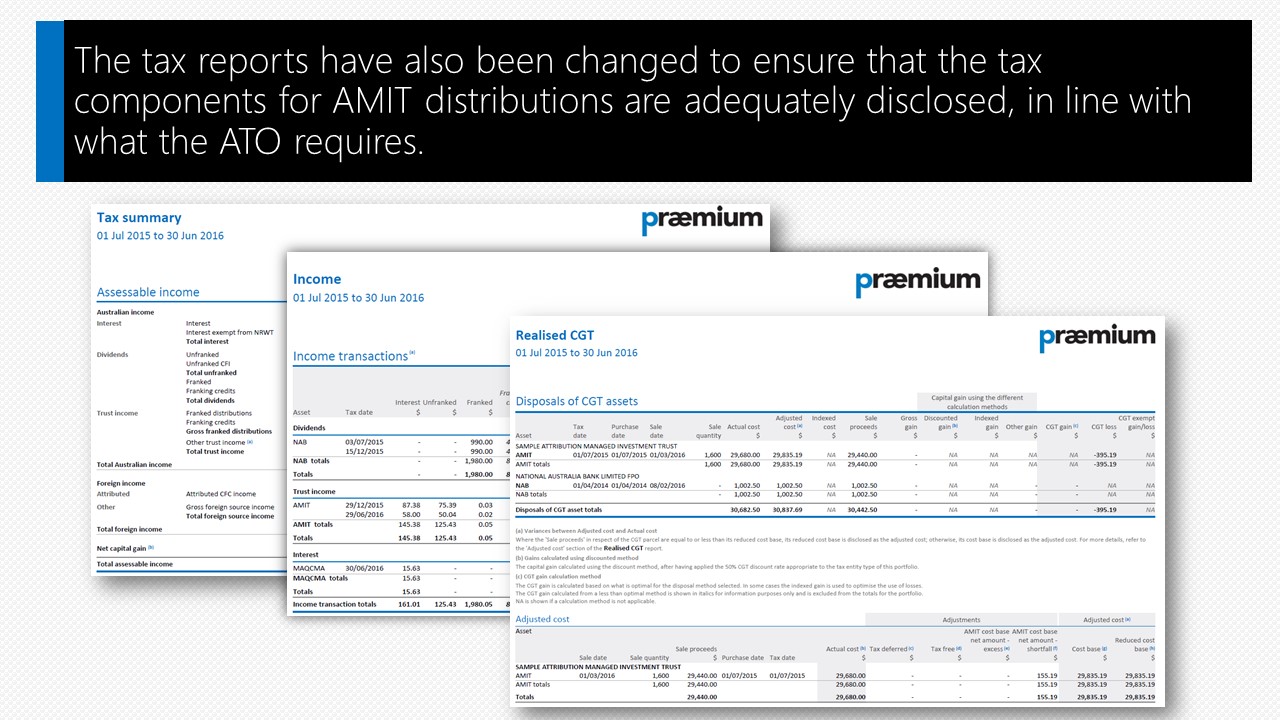

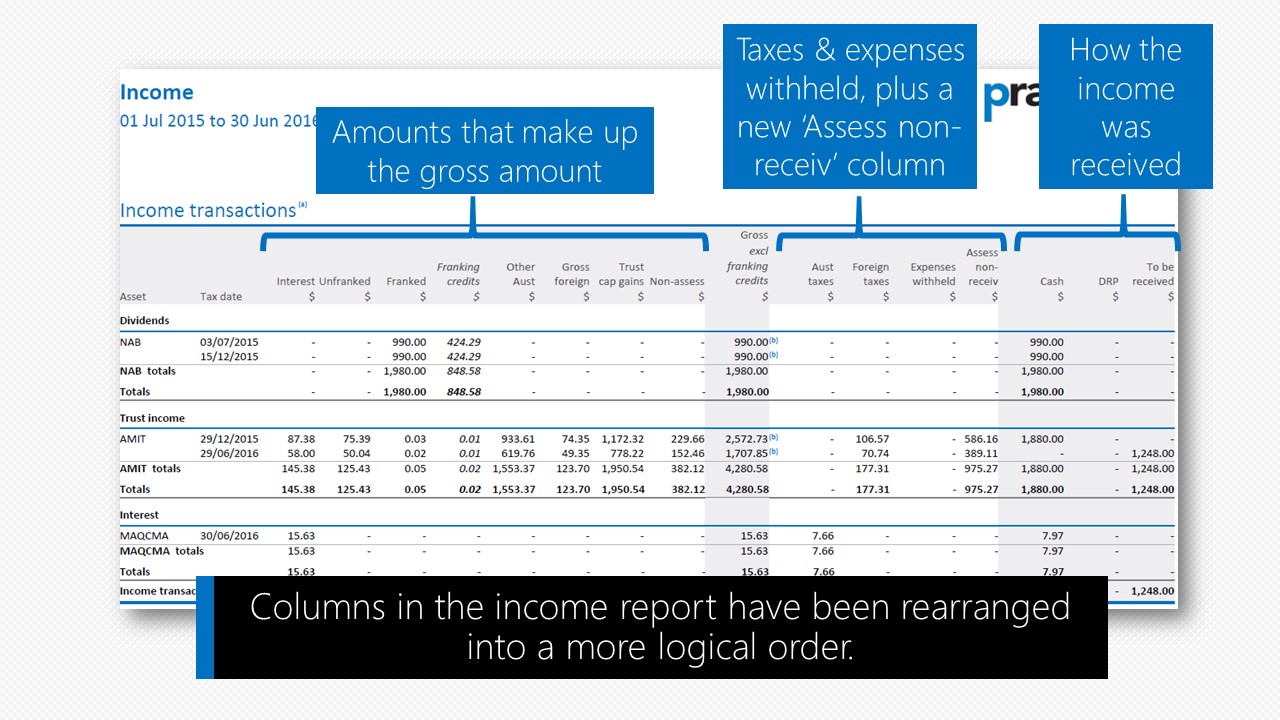

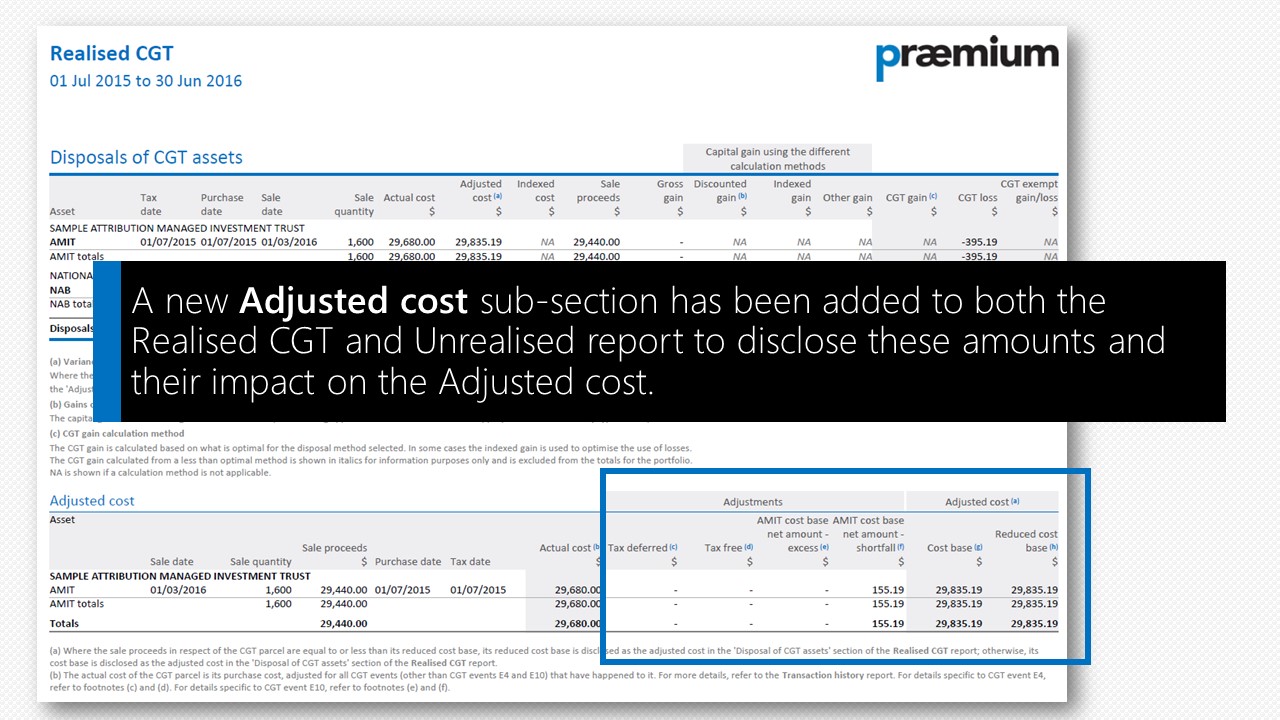

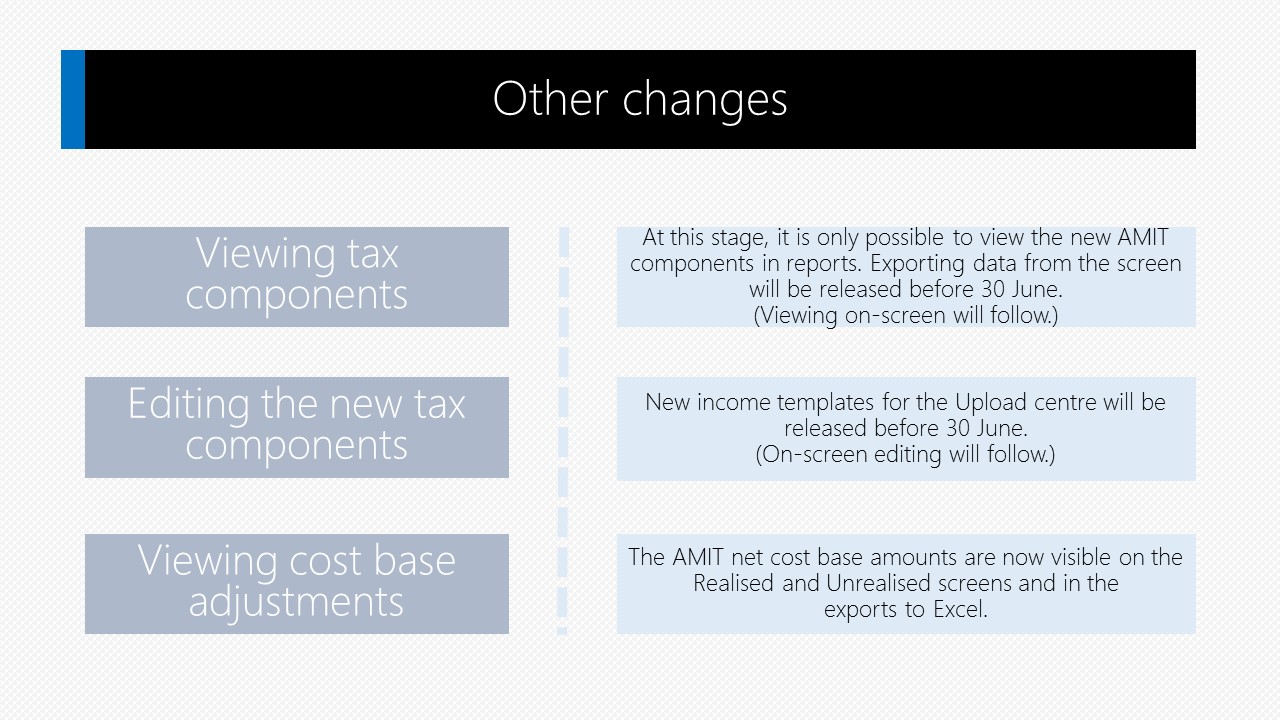

The introduction of the attribution managed investment trust (AMIT) regime, taking effect more widely in the 2016–2017 tax year, has required the addition of new tax components for trust income transactions, as well as new cost-base adjustments for these unit trusts. No action is required from you. We have updated our tax reports accordingly.

Click through the following slides to get an overview of the new AMIT regime and our approach to meeting the new requirements. (Note, the slideshow works best using a new internet browser such as Chrome or Edge.)

|

|

1 / 17

2 / 17

3 / 17

4 / 17

5 / 17

6 / 17

7 / 17

8 / 17

9 / 17

10 / 17

11 / 17

12 / 17

13 / 17

14 / 17

15 / 17

16 / 17

17 / 17

<

>

Click to download a PDF of this slideshow. |

|

New tax components

AMIT

| Tax component name |

Description |

Impact on amount receivable |

AMIT Only? |

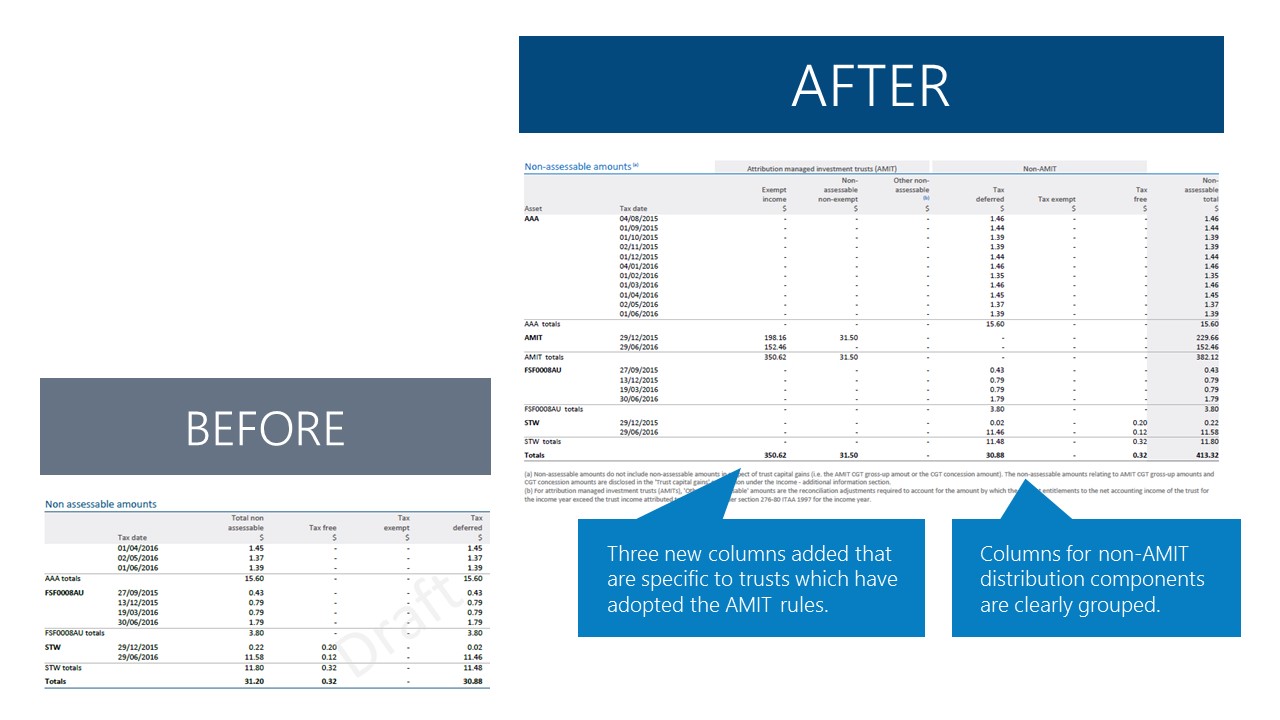

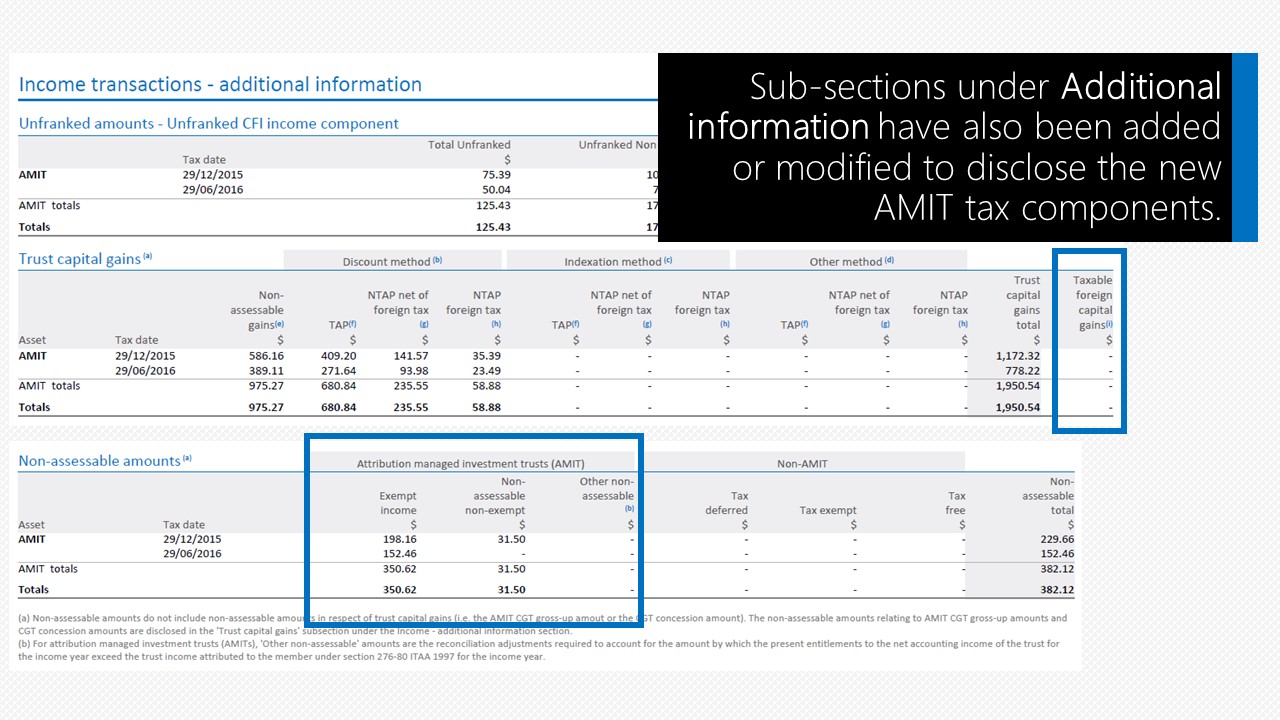

| Exempt income |

The amount of ordinary and statutory income that is exempt income, as listed in section 11-15 ITAA 1997. |

Included |

Yes |

| Non-assess non-exempt |

The amount of ordinary and statutory income that is non-assessable non-exempt income, as listed in section 11-55 ITAA 1997. |

Included

|

Yes |

| Other non-assess |

For AMITs only, the amount by which total income distributed for accounting/trust law purposes in respect of an income year exceeds total attributed income for taxation purposes for that year. This is the complement to 'Assessable non-receivable' in the Amounts withheld (or otherwise non-receivable) section. |

Included

|

Yes |

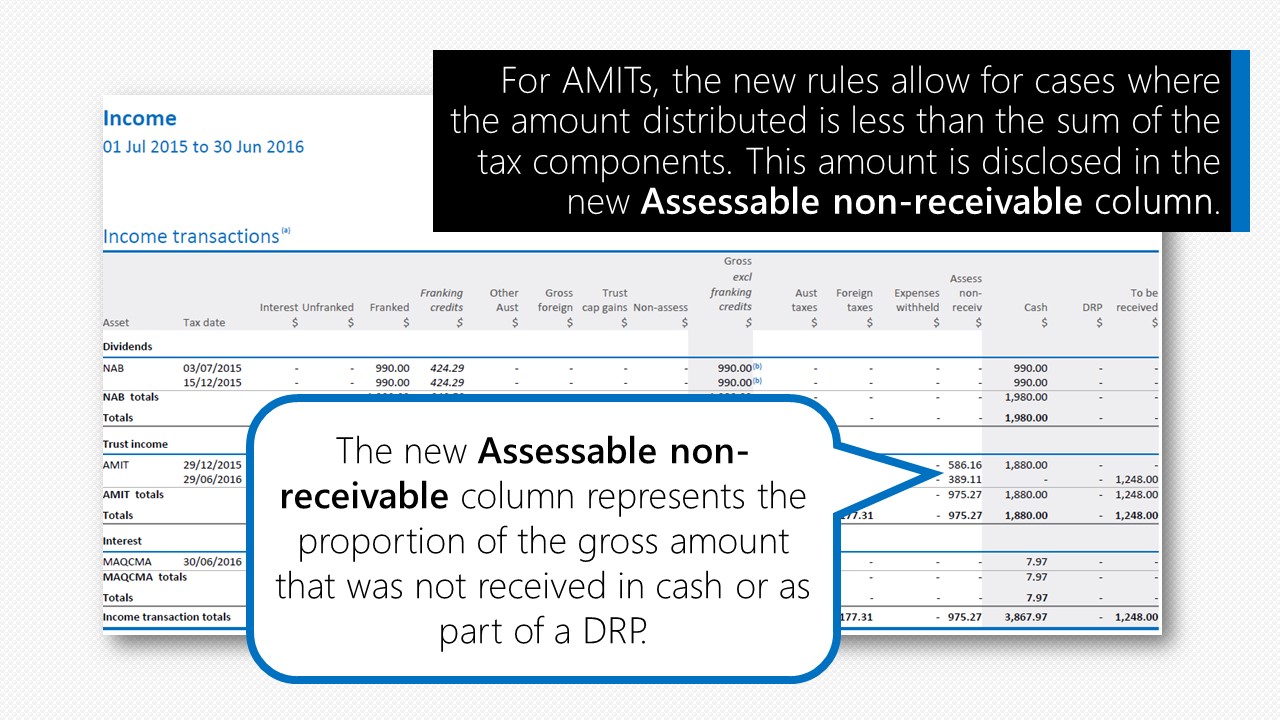

| Assessable non-receivable |

This is essentially a non-cash amount.

For AMITs, this is possible when the amount by which total attributed income for taxation purposes for an income year exceeds total distributed income for accounting/trust law purposes for that year (e.g. MGR 2015-16).

This is the complement to 'Other non-assessable' in the Non-assessable section.

For non-AMITs, this is theamount by which the distribution for taxation purposes for an income year exceeds the distribution for accounting/trust law purposes for that year (e.g. SCG 2015-16). |

Subtracted |

No |

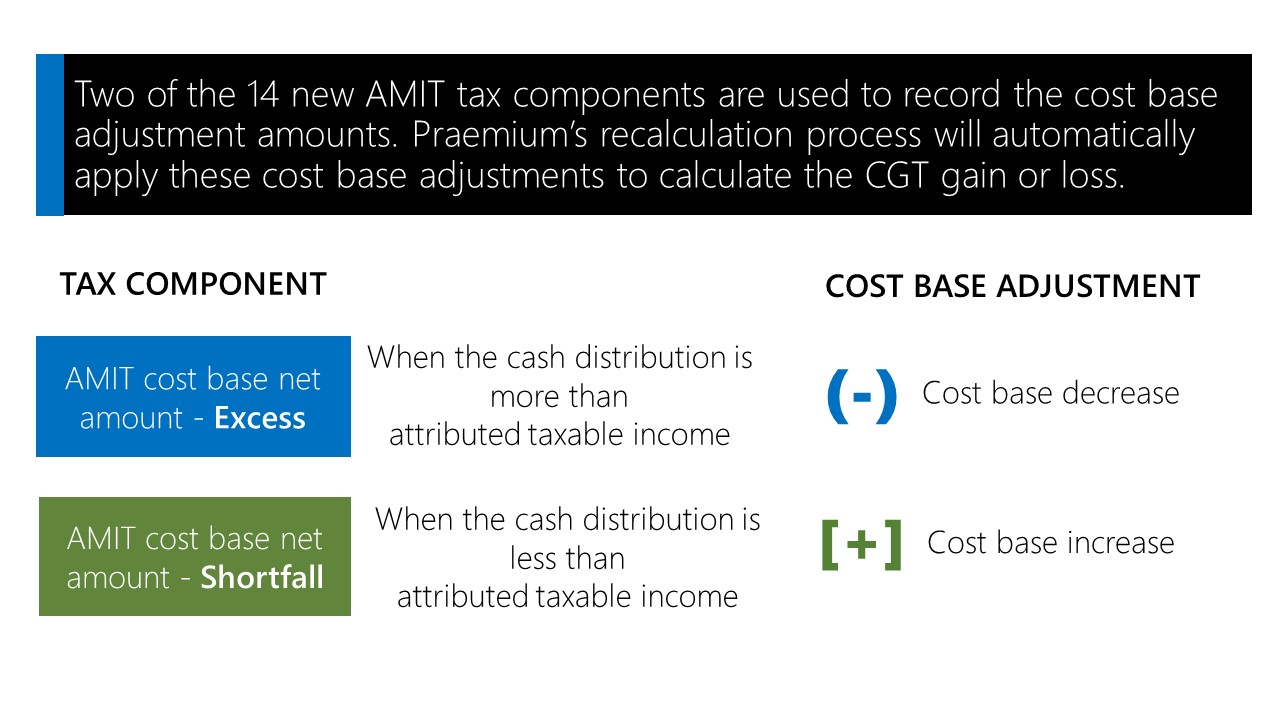

| AMIT cost base net amount - excess |

The excess amount, as calculated under paragraph 104-107C(a) ITAA 1997. Both the cost base and the reduced cost base of the underlying CGT asset are decreased by this amount. |

No impact |

Yes |

| AMIT cost base net amount - shortfall |

The shortfall amount, as calculated under paragraph 104-107C(b) ITAA 1997. Both the cost base and the reduced cost base of the underlying CGT asset are increased by this amount. |

No impact

|

Yes |

Australian income

| Tax component name |

Description |

Impact on amount receivable

|

AMIT Only? |

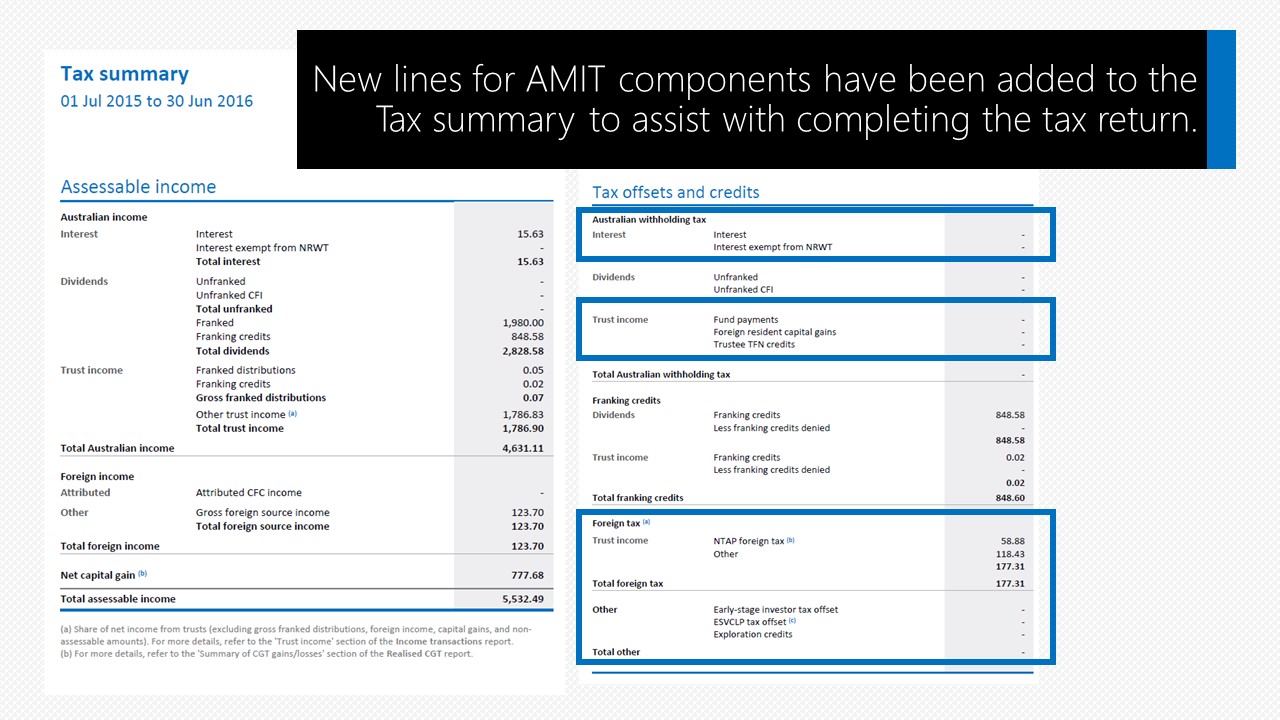

| Interest exempt from NRWT |

Interest that is not subject to non-resident withholding tax. |

Included

|

No |

| Franking credits total |

The amount of the franking credit attached to the franked part of a distribution.

|

No impact

|

No |

Trust capital gains

| Tax component name |

Description |

Impact on amount receivable

|

AMIT Only? |

| Taxable foreign capital gains |

For information purposes only, the total capital gains made in respect of foreign CGT assets. These are stated gross of any foreign tax, exclude the CGT concession amount and AMIT CGT gross up amount, and the discount capital gain is grossed up by doubling it. |

No impact

|

No |

Australian taxes

| Tax component name |

Description |

Impact on amount receivable

|

AMIT Only? |

| Trustee TFN credits |

Includes amount withheld by investment bodies from interest, dividends, and fund payments paid to the trustee. |

Subtracted

|

No |

| Foreign resident CGWT |

The amount of tax withheld by purchasers from foreign resident capital gains payments made to vendor in respect of taxable Australian property (TAP). |

Subtracted

|

No |

Tax offsets

| Tax component name |

Description |

Impact on amount receivable

|

AMIT Only? |

| Early-stage investor |

The amount of any early-stage investor tax offset. |

No impact

|

No |

| ESVCLP |

The amount of any early-stage venture capital limited partnership tax offset. |

No impact

|

No |

| Exploration credits |

The amount of any exploration credit tax offset. |

No impact

|

No |

|

|

|

|

Want to test it for yourself?

We have created a new fictional global asset so that you can include it in a portfolio to do your own testing. The asset code is AMIT and you can add it to your portfolio using the Transaction history screen as you would any other asset.

You will need to recalculate the portfolio to apply the distributions to your test portfolio and generate the tax reports to see the new tax components and cost base adjustments for this fictional asset. Don't forget to delete it from your portfolio when you have finished testing!

|

|

|

|

|

|